Why Your S-Corporation Loss Is Disallowed: Understanding Basis Rules

Many S-corporation owners are surprised when losses are disallowed. Learn how shareholder basis limits deductions and creates long-term tax consequences.

Han S Kim, CPA

3/2/20263 min read

Many S-corporation owners are surprised to learn that a loss shown on their tax return does not automatically reduce their personal tax liability.

The return may reflect a significant loss. The books may document a difficult year. Cash may have left the business. Yet the loss is partially or fully disallowed on the individual return.

When that happens, the explanation is usually straightforward yet poorly communicated: basis.

This article explains why S-corporation losses are frequently disallowed, what basis actually means, and why a return can be technically correct while still creating long-term tax consequences.

Why an S-Corporation Loss Does Not Automatically Reduce Your Taxes

S-corporation income and losses generally pass through to shareholders. That principle is widely understood but incomplete.

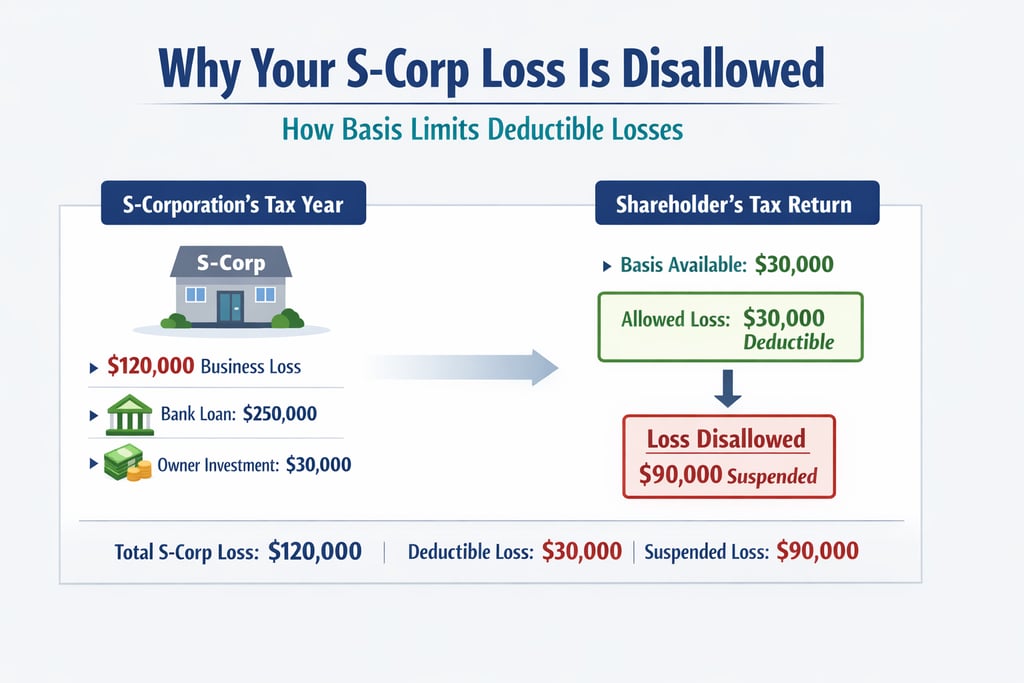

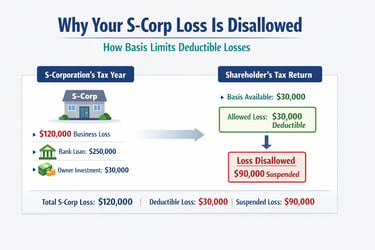

Under the tax law, a shareholder may deduct S-corporation losses only to the extent of their basis in the corporation. Basis functions as a ceiling. Losses exceeding that ceiling are not immediately lost, but they are not currently deductible either.

This distinction matters because:

Tax losses are not equivalent to economic losses

Cash flow does not determine deductibility

The income statement alone does not control the tax result

If basis is insufficient, the loss is suspended regardless of the severity of the business downturn.

What "Basis" Actually Means in an S-Corporation

Basis measures the shareholder's economic risk in the business. For S-corporations, it exists in two forms.

Stock Basis

Stock basis generally increases when the shareholder:

Contributes capital to the S-corporation

Reports taxable income from the S-corporation

Is allocated certain income items

Stock basis generally decreases when the shareholder:

Takes distributions

Is allocated losses

Is allocated nondeductible expenses

Once stock basis is reduced to zero, losses cannot pass through unless debt basis exists.

Debt Basis

Debt basis exists only when there is direct indebtedness from the S-corporation to the shareholder.

This means:

The shareholder lends money directly to the S-corporation

The loan is bona fide

The shareholder is the actual creditor

Debt basis is not created by intent, guarantees, or economic exposure alone. The structure of the debt matters.

This is where most problems arise.

The Most Common Basis Mistake: Entity Debt That Doesn't Count

One of the most frequent and costly misunderstandings involves bank loans.

If a bank lends money to the S-corporation, the loan does not create shareholder basis, even if:

The shareholder personally guaranteed the loan

The shareholder pledged personal assets

The shareholder feels economically responsible for the debt

From a tax perspective, the creditor is the bank, not the shareholder. No direct indebtedness exists between the shareholder and the corporation.

As a result:

The loan increases the corporation's liabilities

It does not increase the shareholder's basis

Losses funded by that debt may be nondeductible

This outcome surprises many business owners because it conflicts with how risk is perceived outside the tax code.

Why Bonus Depreciation Makes the Problem Appear Suddenly

In recent years, large first-year deductions such as bonus depreciation have caused S-corporations to report substantial losses.

These deductions often:

Accelerate losses into a single year

Create significant "paper" losses

Outpace the shareholder's basis

Bonus depreciation does not create basis. It only magnifies the loss.

Consequently, the loss may appear suddenly disallowed, even though the underlying issue existed previously. The depreciation did not cause the problem—it exposed it.

What Happens to Disallowed Losses

When an S-corporation loss exceeds available basis, the excess is suspended.

Suspended losses:

Carry forward indefinitely

Are released only when basis is restored

Do not expire automatically

Basis may be restored through:

Additional capital contributions

Direct shareholder loans

Future taxable income

If basis is never restored, suspended losses can remain unused for years. In some cases, they are effectively stranded because the business structure never changes.

This is why basis errors compound over time.

Why a Return Can Be Correct and Still Cost You Money

Many tax returns are prepared correctly from a compliance standpoint but fail at the structural level.

Common issues include:

No annual basis schedule maintained

Basis not reconciled across years

Distributions exceeding basis without explanation

Loans not reviewed for proper tax characterization

When this happens, the return may be technically accurate while quietly limiting deductions year after year.

By the time the issue is identified, correction often requires amended returns, debt restructuring, or accepting that prior losses cannot be utilized as expected.

How This Should Be Addressed Before the Loss Appears

Basis issues are most manageable before losses accumulate.

This typically involves:

Tracking basis annually, not retroactively

Reviewing how business debt is structured

Coordinating distributions with basis levels

Understanding how large deductions affect subsequent years

These steps constitute forward-looking tax planning, not last-minute compliance work.

The Bottom Line

An S-corporation loss does not guarantee a tax benefit.

Basis controls deductibility. When basis is ignored or misunderstood, losses become suspended, delayed, or effectively unusable.

This represents one of the clearest examples of how a return can be technically correct while still producing an unfavorable outcome.

For S-corporation owners, understanding basis is not optional—it is foundational.

This article is for educational purposes only. Tax outcomes depend on individual facts, entity structure, and prior-year activity. Planning decisions should be evaluated before filing.

Contact

Get in touch for expert advice.

Follow

Work with me

info@hskcpa.com

(949) 614-1133

© 2026. All rights reserved.

Privacy Policy | Terms of Use

From tax filing to tax strategy, the next step is a conversation.

In-person consultations available: Los Angeles & Irvine (by appointment only)

한국어 상담 가능