Should My LLC Be an S Corp? The California Break-Even Analysis Most CPAs Skip

California’s gross receipts fee and 1.5% S Corp franchise tax change the break-even math. Here is how to run the actual numbers before making the S Corp election.

Han S Kim, CPA

6/2/20267 min read

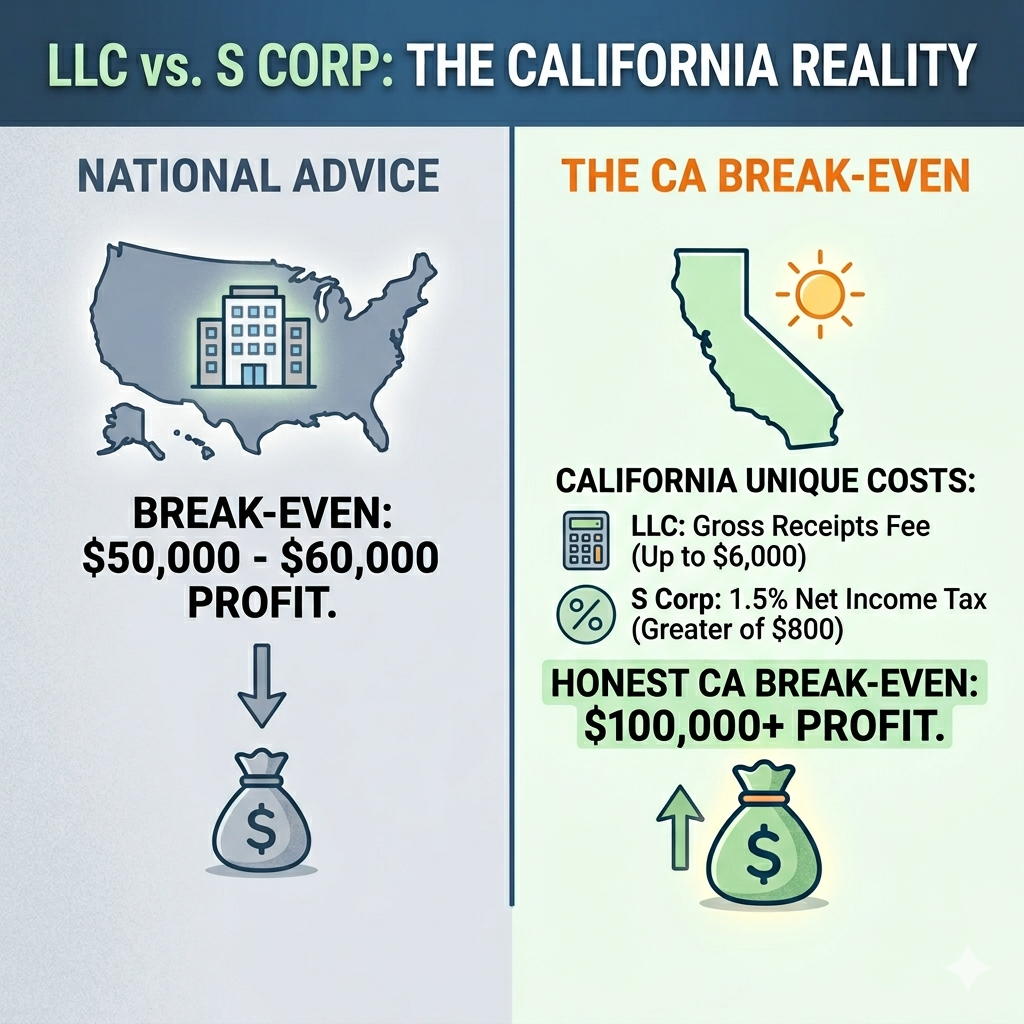

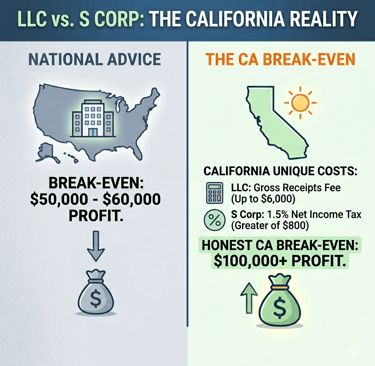

Most content on this topic quotes a national break-even of $50,000 to $60,000 in net profit. That figure compares federal self-employment tax savings against generic compliance costs. It ignores California entirely. California imposes costs that do not exist in other states, and it also eliminates a cost that LLC owners pay in those same states. Run the California numbers and the answer is different.

What the Election Actually Is

This is a tax classification change, not a legal one. Your LLC stays an LLC with the California Secretary of State. What changes is how the IRS taxes your income.

As a single-member LLC taxed as a disregarded entity, every dollar of net profit flows to Schedule C and gets hit with self-employment tax at 15.3% up to the Social Security wage base ($184,500 in 2026), then 2.9% on everything above it. There is no mechanism to split the income.

When you elect S Corp treatment by filing IRS Form 2553, you become an employee of your own company. You pay yourself a W-2 salary. That salary is subject to payroll taxes. The profit above your salary flows to you as a distribution and escapes self-employment tax. The gap between your salary and your total profit is where the savings come from.

For new entities, the election must be filed within two months and 15 days of formation to take effect in the current tax year. For existing calendar-year LLCs, the deadline is March 15 of the year in which the election is to apply. Miss both windows and you can pursue a late election under Rev. Proc. 2013-30, but that requires demonstrating reasonable cause and the IRS does not approve every request. California automatically recognizes the federal election; no separate state-level filing is required.

What California Actually Charges

California charges a flat $800 annual franchise tax on every LLC regardless of profit. Above $250,000 in gross revenue, it also charges a gross receipts fee on a tiered schedule. At $250,000 to $499,999 gross, that fee is $900. At $500,000 to $999,999, it is $2,500. At $1,000,000 to $4,999,999, it is $6,000.

When your LLC elects S Corp treatment, the gross receipts fee disappears. California instead charges the greater of $800 or 1.5% of the entity’s net income.

Consider a hypothetical. Call her Sarah, a management consultant in Los Angeles operating as a single-member LLC. In 2026, she projects $250,000 in gross revenue and $150,000 in net profit. As a default LLC, Sarah pays $800 in franchise tax plus a $900 gross receipts fee, totaling $1,700 in California entity-level taxes. If she elects S Corp status, California charges the greater of $800 or 1.5% of $150,000. One and a half percent of $150,000 is $2,250, which exceeds $800, so her California entity tax is $2,250. The S Corp election costs her $550 more at the California level than her default LLC structure.

This is what national calculators miss. The S Corp election does not produce state-level savings in California for a consultant in this income range. It produces a state-level tax increase. The federal savings have to more than cover this.

The Federal Savings Calculation

Back to Sarah. Self-employment tax applies to 92.35% of net profit, a statutory adjustment. At $150,000 net profit, that is $138,525 subject to the 15.3% rate. Her self-employment tax as a default LLC is approximately $21,194.

If Sarah elects S Corp status and pays herself a reasonable W-2 salary of $80,000, combined payroll taxes (employer and employee share) on that salary total approximately $12,240. The remaining $70,000 flows as a distribution with no self-employment tax. Her federal employment tax cost drops from roughly $21,194 to roughly $12,240, a savings of approximately $8,954.

This is a hypothetical illustration. Actual results depend on the salary amount, the applicable Social Security wage base, other income on the return, and deductions available. The numbers change with the inputs.

What the Election Costs

Sarah now runs formal payroll every pay period. She registers with the California Employment Development Department, withholds state income tax, remits SDI, and files quarterly payroll returns. Payroll processing through a third-party service runs roughly $100 to $150 per month, meaning $1,200 to $1,800 annually.

Her federal return now requires Form 1120-S in addition to her individual return. California requires Form 100S. An incremental tax preparation fee of $800 to $1,500 per year is reasonable in the California market, though this varies by preparer and practice complexity.

Total added compliance cost estimate for this hypothetical: $2,000 to $3,300 per year.

The Honest California Break-Even

Using Sarah’s numbers:

Federal SE tax savings: approximately $8,954. California state tax increase: approximately $550. Net tax benefit before compliance costs: approximately $8,404. Compliance costs at midpoint: approximately $2,650. Net annual benefit: approximately $5,754.

At $150,000 net profit with an $80,000 salary, the election produces a positive result. But the margin is narrower than national figures suggest, and it only gets worse at lower income levels.

Run the same analysis at $80,000 net profit. The federal savings narrow because the salary and total profit are closer together, which leaves less untaxed distribution income. The California state tax increase becomes proportionally more painful because 1.5% of $80,000 net income ($1,200) compares to the $800 flat fee for a sub-$250,000 gross LLC, a difference of only $400. Compliance costs do not shrink because you still need payroll, Form 1120-S, and Form 100S.

The honest California break-even for a service-based consultant is closer to $100,000 to $120,000 in net profit, not the $50,000 to $60,000 figure in national guides. The exact threshold shifts based on your gross revenue relative to the fee tiers, the salary you set, and the compliance costs you actually incur.

When the Election Makes Things Worse

Variable income. The S Corp election requires running payroll and paying a reasonable salary even in low-income years. If your practice earns $60,000 net profit in a slow year and your salary is documented at $70,000, you have a cash flow problem and a compliance problem simultaneously. The IRS does not suspend the reasonable compensation requirement because revenue dropped.

First-year businesses. Net profit projections for a new consulting practice are unreliable. Electing S Corp status in year one and then falling short of the break-even threshold means you absorbed compliance costs with no tax benefit. Reversing the election requires IRS approval and is not guaranteed.

High revenue, low margin. A consultant with $400,000 in gross revenue and $60,000 in net profit after expenses faces a different calculation. The S Corp election does eliminate the gross receipts fee, which helps. But the net income is too thin to generate meaningful federal savings once compliance costs are subtracted.

Eligibility issues. S Corp eligibility requires 100 or fewer shareholders, all of whom must be U.S. citizens or permanent residents. Non-resident alien owners disqualify the entity entirely. This rarely affects solo California consultants but should be confirmed before filing.

The Variable That Decides Everything

The salary you set drives the entire outcome. Set it too low and the IRS reclassifies distributions as wages, which eliminates the tax benefit and generates back taxes plus penalties. Set it too high and you eliminate the savings you were trying to create.

Reasonable compensation is not a percentage of profit. It is what you would pay someone else to do what you do, supported by wage data for your industry and your market, and documented before you file. Getting this wrong is not a minor error. It is the most common reason an S Corp election produces an audit notice rather than a tax savings. The compensation analysis and its connection to retirement planning is covered in more detail in Your S Corporation Salary Fixes One Problem. It Creates Another One Nobody Mentions.

The Risk Cheap Preparers Create Every Year

Reasonable compensation gets most of the attention. Basis tracking causes more silent damage.

Every S Corp shareholder has a stock basis account. It starts with your initial capital contribution and adjusts every year: up for income allocated to you on the K-1, down for losses and distributions. Distributions are tax-free only to the extent of your basis. Take a distribution above your basis and the excess is taxable as a capital gain, regardless of whether you knew the basis was exhausted.

Most owners never see this problem coming because no one told them it existed. A preparer who files your Form 1120-S without maintaining a running basis schedule is leaving you exposed. The IRS does not send a warning. It shows up in an audit, often years after the distribution was taken, when reconstructing basis from scratch is expensive and sometimes impossible.

The risk compounds over time. An S Corp that passes through losses in early years depletes basis faster than owners expect. A cash distribution taken in a profitable year, after years of losses, can push an owner into a taxable gain they did not anticipate and the preparer did not flag.

This is not a hypothetical. It is one of the most common and costly errors in S Corp tax preparation, and it is largely invisible until the damage is done. Before electing S Corp status, confirm that whoever prepares your return will maintain a basis schedule annually. If they cannot explain what that means, find someone who can.

The Decision Framework

Four questions in order:

Is your California net profit consistently above $100,000? If not, the election likely costs more than it saves in California.

Is that profit reasonably stable from year to year? If income swings unpredictably, the payroll obligation creates real exposure in low-income years.

Are you prepared to run formal payroll, file two additional tax returns, and document a defensible reasonable salary? These are ongoing obligations, not one-time tasks.

Have you confirmed eligibility? No foreign owners, no more than 100 shareholders, one class of membership interest.

If the answers are yes, the election is worth modeling with your specific numbers. The national break-even figure is not wrong in the abstract. It is wrong for California. Using it without adjusting for the state fee structure can lead to a structure that costs more in total than staying on Schedule C.

Whether the S Corp election makes sense depends on your specific profit level, revenue structure, compensation range, and California fee exposure. Getting it wrong in either direction has real cost. If you want an honest assessment of whether the election works for your situation, I work with California consultants and business owners through my tax advisory services page on exactly these decisions.

Contact

Get in touch for expert advice.

Follow

Work with me

info@hskcpa.com

(949) 614-1133

© 2026. All rights reserved.

Privacy Policy | Terms of Use

From tax filing to tax strategy, the next step is a conversation.

In-person consultations available: Los Angeles & Irvine (by appointment only)

한국어 상담 가능